Economics resources for Queensland high school students, teachers, and everyone else

Unit 1 Topic 1: The Basic Economic Problem

Video Overview of Unit 1 Topic 1: linking the content to the syllabus

PART 1: WHAT IS ECONOMICS?

Syllabus: Describe the basic economic problem of relative scarcity and the need for decision-making by individuals, businesses and governments at local, state, national and international levels.

Economics is the study of how humans make decisions in the face of scarcity.

These can be individual decisions, family decisions, business decisions or societal decisions. If you look around carefully, you will see that scarcity is a fact of life.

Scarcity means that human wants for goods, services and resources exceed what is available.

Resources, such as labour, tools, land, and raw materials are necessary to produce the goods and services we want but they exist in limited supply. Of course, the ultimate scarce resource is time - everyone, rich or poor, has just 24 hours in the day to try to acquire the goods they want.

At any point in time, there is only a finite amount of resources available.

Think about it this way: in November 2021, the labour force in Australia contained over 13,177,300 workers, according to the Australian Bureau of Statistics (ABS)[1]. Similarly, the total area of the Australia is 7,692,020 square kilometres[2]. These are large numbers for such crucial resources, however, they are limited. Because these resources are limited, so are the numbers of goods and services we produce with them.

Let’s delve into the concept of scarcity a little deeper, because it is crucial to understanding economics.

The Problem of Scarcity

Think about all the things you consume: food, shelter, clothing, transportation, healthcare, and entertainment. How do you acquire those items? You do not produce them yourself. You buy them. How do you afford the things you buy? You work for pay. Or if you do not, someone else does on your behalf. Yet most of us never have enough to buy all the things we want. This is because of scarcity.

So how do we solve it? Every society, at every level, must make choices about how to use its resources.

Families must decide whether to spend their money on a new car or a fancy vacation. Towns must choose whether to put more of the budget into police and fire protection or into the school system. Nations must decide whether to devote more funds to national defence or to protecting the environment. In most cases, there just isn’t enough money in the budget to do everything.

So why do we not each just produce all of the things we consume? The simple answer is most of us do not know how, but that is not the main reason. When you study economics, you will discover that the obvious choice is not always the right answer—or at least the complete answer. Studying economics teaches you to think in a different of way.

Think back to pioneer days, when individuals knew how to do so much more than we do today, from building their homes, to growing their crops, to hunting for food, to repairing their equipment. Most of us do not know how to do all—or any—of those things. It is not because we could not learn. Rather, we do not have to. The reason why is something called the division and specialization of labour, a production innovation first put forth by Adam Smith, in his book, The Wealth of Nations.

PART 2: The Division of and Specialisation of Labour

The formal study of economics began when Adam Smith (1723–1790) published his famous book The Wealth of Nations in 1776. Many authors had written on economics in the centuries before Smith, but he was the first to address the subject in a comprehensive way.

In the first chapter, Smith introduces the division of labour, which means that the way a good or service is produced is divided into a number of tasks that are performed by different workers, instead of all the tasks being done by the same person.

To illustrate the division of labour, Smith counted how many tasks went into making a pin: drawing out a piece of wire, cutting it to the right length, straightening it, putting a head on one end and a point on the other, and packaging pins for sale, to name just a few. Smith counted 18 distinct tasks that were often done by different people—all for a pin, believe it or not!

Modern businesses divide tasks as well. Even a relatively simple business like a restaurant divides up the task of serving meals into a range of jobs like top chef, sous chefs, less-skilled kitchen help, servers to wait on the tables, a greeter at the door, janitors to clean up, and a business manager to handle paychecks and bills—not to mention the economic connections a restaurant has with suppliers of food, furniture, kitchen equipment, and the building where it is located.

A complex business like a large manufacturing factory, or a hospital can have hundreds of job classifications.

Why the Division of Labour Increases Production

When the tasks involved with producing a good or service are divided and subdivided, workers and businesses can produce a greater quantity of output. In his observations of pin factories, Smith observed that one worker alone might make 20 pins in a day, but that a small business of 10 workers (some of whom would need to do two or three of the 18 tasks involved with pin-making), could make 48,000 pins in a day. How can a group of workers, each specializing in certain tasks, produce so much more than the same number of workers who try to produce the entire good or service by themselves? Smith offered three reasons.

First, specialisation in a particular small job allows workers to focus on the parts of the production process where they have an advantage.

People have different skills, talents, and interests, so they will be better at some jobs than at others. The particular advantages may be based on educational choices, which are in turn shaped by interests and talents. Only those with medical degrees qualify to become doctors, for instance. For some goods, specialization will be affected by geography and climate—it is easier to be a wheat farmer in rural Western Australia than in Cairns, but easier to run a tourist hotel in Cairns than in the Western Australian wheatbelt. Whatever the reason, if people specialise in the production of what they do best, they will be more productive than if they produce a combination of things, some of which they are good at and some of which they are not.

Second, workers who specialise in certain tasks often learn to produce more quickly and with higher quality.

This pattern holds true for many workers, including assembly line laborers who build cars, stylists who cut hair, and doctors who perform heart surgery. In fact, specialised workers often know their jobs well enough to suggest innovative ways to do their work faster and better. A similar pattern often operates within businesses. In many cases, a business that focuses on one or a few products (sometimes called its “core competency”) is more successful than firms that try to make a wide range of products.

Third, specialisation allows businesses to take advantage of economies of scale, which means that for many goods, as the level of production increases, the average cost of producing each individual unit declines.

For example, if a factory produces only 100 cars per year, each car will be quite expensive to make on average. However, if a factory produces 50,000 cars each year, then it can set up an assembly line with huge machines and workers performing specialized tasks, and the average cost of production per car will be lower.

The ultimate result of workers who can focus on their preferences and talents, learn to do their specialised jobs better, and work in larger organisations is that society (as a whole) can produce and consume far more than if each person tried to produce all their own goods and services.

The division and specialisation of labour has been a force against the problem of scarcity.

Trade and Markets Specialisation only makes sense, though, if workers can use the pay, they receive for doing their jobs to purchase the other goods and services that they need.

In short, specialisation requires trade.

Instead of trying to acquire all the knowledge and skills involved in producing all of the goods and services that you wish to consume, the market allows you to learn a specialised set of skills and then use the pay you receive to buy the goods and services you need or want. This is how the economy has evolved in modern society.

PART 3: Why Study Economics?

Now that we have gotten an overview on what economics studies, let’s quickly discuss why you are right to study it. Economics is not primarily a collection of facts to be memorized, though there are plenty of important concepts to be learned.

Economics is better thought of as a collection of questions to be answered or puzzles to be worked out. Most importantly, economics provides the tools to work out those puzzles. If you have yet to be bitten by the economics “bug,” there are other reasons why you should study economics. Virtually every major problem facing the world today, from global warming, to world poverty, to the conflicts in Syria, Afghanistan, and Somalia, has an economic dimension. If you are going to be part of solving those problems, you need to be able to understand them. Economics is crucial. It is hard to overstate the importance of economics to good citizenship. You need to be able to vote intelligently on budgets, regulations, and laws in general.

When the Australian Government had to make tough economic and financial decisions during the “Covid lockdowns” in 2020, what were the issues involved? Did you know? A basic understanding of economics makes you a well-rounded thinker. When you read articles about economic issues, you will understand and be able to evaluate the writer’s argument. When you hear classmates, co-workers, or political candidates talking about economics, you will be able to distinguish between common sense and nonsense. You will find new ways of thinking about current events and about personal and business decisions, as well as current events and politics. The study of economics does not dictate the answers, but it can illuminate the different choices.

Source: https://openstax.org/books/principles-economics-2e/pages/1-introduction

Footnotes

[2]https://info.australia.gov.au/about-australia/our-country/the-australian-continent

Factors of Production

Syllabus: Classify the factors of production (land, labour, capital and entrepreneurial ability) and link these to income (rent, wages, interest and profit)

Let's start with a question....

WHAT are the four factors of production?

Answer: Land, Labour, Capital, and Enterprise (or Entrepreneurship).

Easy! You've learnt this in class and can explain each of the the factors.

And you know that the four factors are all required (in different combinations)

to make different goods and services.

So let's go deeper ....

Economic Activity versus Economic Growth

(and the factors of production)

I believe that being able to distinguish between economic activity and economic growth this is one of the most important concepts that you need to understand in your study of economics.

Economic activity represents the cyclical changes in the economy (also referred to as the 'short-run').

-

Sometimes economies are expanding / expansionary phase (as households, firms and government buy more goods and services), and sometimes economies are contracting / contractionary phase (as we buy less stuff).

-

At any point in time, the available factors of production are somewhat fixed. For example:

-

available labour is determined by the quantity of labour available to work with appropriate skills, knowledge and experience;

-

land resources are relatively scarce, and generally allocated to a certain production function (eg. agriculture or mining);

-

capital such as machinery and factory size is relatively fixed at a point in time.

-

So the short-run refers to the level of output an economy with the currently available factors of production.

In other words, the amount of possible output with a fixed amount of factors of production.

Factors of production may not always be utilised to their full capacity

-

When the level of demand in the economy is high, we will see that the available factors of production will be close to fully engaged in the process of making goods and services. For example, labour will have jobs, and we see this when the unemployment rate is low. Factories will be working near to full capacity, and maybe doing overtime shifts. Economy is in an expansionary phase of the economic cycle. If firms can't produce enough G+S to meet demand, they will tend to increase prices of the available stock to maximise profit. We call this demand-push inflation (more on this later).

-

BUT, When the level of demand is low, the available factors of production will not be used to their full extent. For example, some workers will lose their jobs, and the unemployment rate will rise. Factories will cut back on production output, and some machines will not produce to their production capacity. So we will see a contraction in the level of economic activity.

The 'ups and downs' in the economy represents changes in the level economic activity, and we refer to these changes as expansionary and contractionary.

Economic activity :: data examples

Economic growth is a sustained increase in the level of output, caused by structural growth in the economy (the long-run).

Over time, economies experience an increase in the quantity and quality of the factors of production. For example:

-

Population increases leads to an increase in the quantity of labour

-

Improvements in education and training improves the quality of labour, and workers tend to be more efficient (or productive) in their work.

-

Improvements in technology can increase the level of output given the available resources (factors of production).

-

An increase in capital investment (firms purchasing goods and services - such as additional machinery - to increase the production of final goods and services).

-

What is an example that you can think of?? Eg. how can we improve our land resources to increase agricultural output?

Economic growth occurs when an economy:

-

Increases output due to an increase in the available factors of production; and/or

-

Improves productivity - An increase in output the available for a given quantity of the factors of production (factor inputs). Productivity improvements occur when higher quality factor inputs are used (eg. more efficient technology, smarter people etc).

-

Experiences a sustained increase in demand for goods and services, influenced by factors such as population increase, greater levels of international trade etc.

Given the relative scarcity of factors of production, economists end to argue that improving productivity is the critical step for economic growth - it means that we are using the current factors of production in a more efficient way. That means that we can leave some factors - resources such as minerals in the ground - so that future generations can access these factors for future production.

So the long-run refers to the situation where there is a change (generally an increase or improvement) in at least one of the factors of production. Economies generally exhibit long-run - or structural - economic growth, even though we will experience 'up and downs' in the level of economic activity in the short-run.

Source: Andrew Norton

Source: Reserve Bank of Australia

Source: International Monetary Fund

The Production Possibilities Curve:

economic activity and economic growth

Syllabus:

-

Identify assumptions and use the production possibility curve to explain, by illustrating in diagrammatic form, the concepts of scarcity, choice, opportunity cost, trade -offs, underutilisation of resources, efficiency, productivity, unemployment and economic growth.

-

Analyse and evaluate the production possibility curve to show the effects of different economic events, e.g. improvements in health, education or productivity of labour, asymmetric technology advances, war and famine.

The Production Possibilities Curve (PPC) is the first economic model that you will learn in QCE Economics.

In this section, I will focus on how the PPC can be used to illustrate changes in economic activity (short-run / cyclical) and economic growth (long-run / structural) - see the section above to review these concepts.

This will also be important for later in Unit 1 when you learn about models for economic (business) cycles - all economic models are connected!

If you want to review your calculations of changes in production possibilities, then scroll down for an interactive from our friends at econgraphs.org

Image 1: Production possibilities curve

Economic activity and the PPC

The production decisions of goods and services in an economy falls into two camps: to produce capital (or intermediate) goods and services OR to produce consumer (or final) goods and services.

Each economy will make a choice of how to distribute available factors of production to suit the needs and wants of economic stakeholders who purchase goods and services:

-

Consumer goods and services for households

-

Capital goods and services for firms and government

The PPC represents the maximum output possible with the current amounts of the factors of production.

At a point in time, the factors of production are considered fixed in quantity and quality. In economics, we call this the short-run. This is a really important term - make sure that you remember it.

Therefore, the maximum level of output in the short-run would be any point along the PPC. But remember: it is a possibility!

When total (aggregate) demand from economic stakeholders (household, firms and governments) is high, economic activity is expansionary, and firms will respond by increasing production, until all factors of production are fully employed.

This is represented by a level of output that is on the PPC itself (eg point A in image 1 above).

But once at full employment / production on the PPC, firms will struggle to further increase output - they are constrained by the relative scarcity of the factors of production.

When an economy experiences contractionary economic activity, production levels may decrease, but the PPC doesn't change.

During an economic downturn (contractionary economic activity), firms will respond by reducing output. Firms generally want to produce only the amount of goods and services to meet demand. They don't want to have unsold stock sitting in warehouses. Nor do they want to employ staff when there isn't enough work available. So they will reduce output to meet demand, and this means that the available factors of production are not fully utilised in creating output.

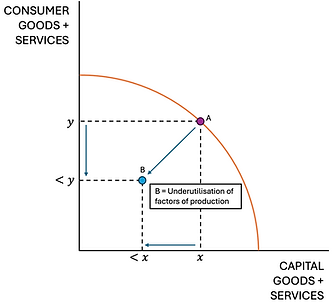

In image 2, this change is demonstrated as a shift in output of consumer goods and services from a value of y to a value less than y, and same for capital goods and services (from x to <x). Total production has decreased from point A to point B.

Image 2: Change in production output in a contractionary economy

It is important to note that the theoretical production possibilities are unchanged.

We still have the factors of production available to produce output anywhere on the PPC, but a decision has been made to decrease output to suit a change in the level of demand in the economy.

Concluding points:

-

Changes in economic output in the short-run (eg from point A to point B) are primarily influenced by changes in demand (purchasing of goods and services by households, firms and governments).

-

The amount of combined purchases across the economy is called Aggregate Demand (more on this later).

-

If Aggregate Demand falls, the economy is contracting.

-

If Aggregate Demand is increasing, the economy is expanding.

-

The fluctuations in the level of of Aggregate Demand is called cyclical economic activity.

Economic growth occurs when there is an increase in the quantity or quality of the factors of production

Let's start with an example.

Since the 1300's, The Netherlands has increased its available land mass by nearly 20%, and most of it with pretty simple technology by today's standards!

You can read more about how they did it here.

From an economics perspective, the first step in the improvement in factors of production would have been the organisation of the major projects - individual landowners working together for the mutual benefits from the improvements.

-

We can call this enterprise / entrepreneurship in our factors of production framework.

-

The increase in land would yield an increase in output (supply) of goods and services. In this instance, likely an increase in agricultural production.

-

The increasing output would also require an increase in labour, which in the short-term is best achieved through migration.

-

Then once you hit an output ceiling, you can increase the quality or quantity of capital - use more machines instead of labour.

In The Netherlands agricultural production continues to increase through the use of greenhouses and hydroponic production methods (capital). They are the second largest exporter of agricultural products in the world, which is pretty incredible for a relatively small country!

The PPC will shift outwards when there is an increase in the quantity or quality of the factors of production

An outward shift of the PPC represents structural, long-run economic growth

We know from the examination of cyclical economic activity earlier that the short-run is where all factors of production are fixed in quality and quantity.

The long-run is where at least one (but likely all) of the factors of production are variable in quantity or quantity.

When an economy, increases the quantity or quality of factors of production, then all production possibilities increase, hence the outward shift of the PPC.

Image 3 illustrates this: the original PPC (and production at point A) is the orange curve. As factors of production increase, the curve shifts outwards (blue curve). No production decisions are yet made - all we know is that we have more inputs, or that we use our inputs more efficiently to create more output. An economy could decide to produce in any combination on the blue curve, and overall output is higher.

Image 3: Outward shift of PPC represents economic growth

The decision to produce at point B would be determined by demand factors such as consumer preference.

At production point B:

-

Production of consumer goods and services has increased from y to y1

-

Production of capital goods and services has increased from x to x1

In the long-run, there is no opportunity cost connected to the decision to increase production of either category of goods. The increase in output is due to either an increase in factor inputs - this is what we call structural (or long-run) economic growth.

Concluding points:

The level of economic activity (short-run) is generally determined by level of Aggregate Demand in the economy. It will experience expansionary and contractionary phases. It is cyclical in nature.

Economic growth (long-run) occurs when there is a sustained increase in level of output in an economy. It is structural in nature. We focus on the longer term trend, rather than short-term fluctuations.

Economic growth occurs through:

-

an improvement in quality of factor inputs - productivity improvements (more output for the same quantity of factor inputs)

-

an increase in the quantity of factor inputs - eg. more population leads to more work undertaken, which leads to increased output

-

A sustained increase in demand for goods and services, influenced by factors such as population increase, greater levels of international trade etc.

An outwards shift of the PPC represents structural (long-run) economic growth.

Thanks to econgraphs.org for creating this open source interactive of the Production Possibilities Curve